A multiple-bubble descriptive model of bitcoin pricePreliminary version

[ click on the graph for a full-size version. ]

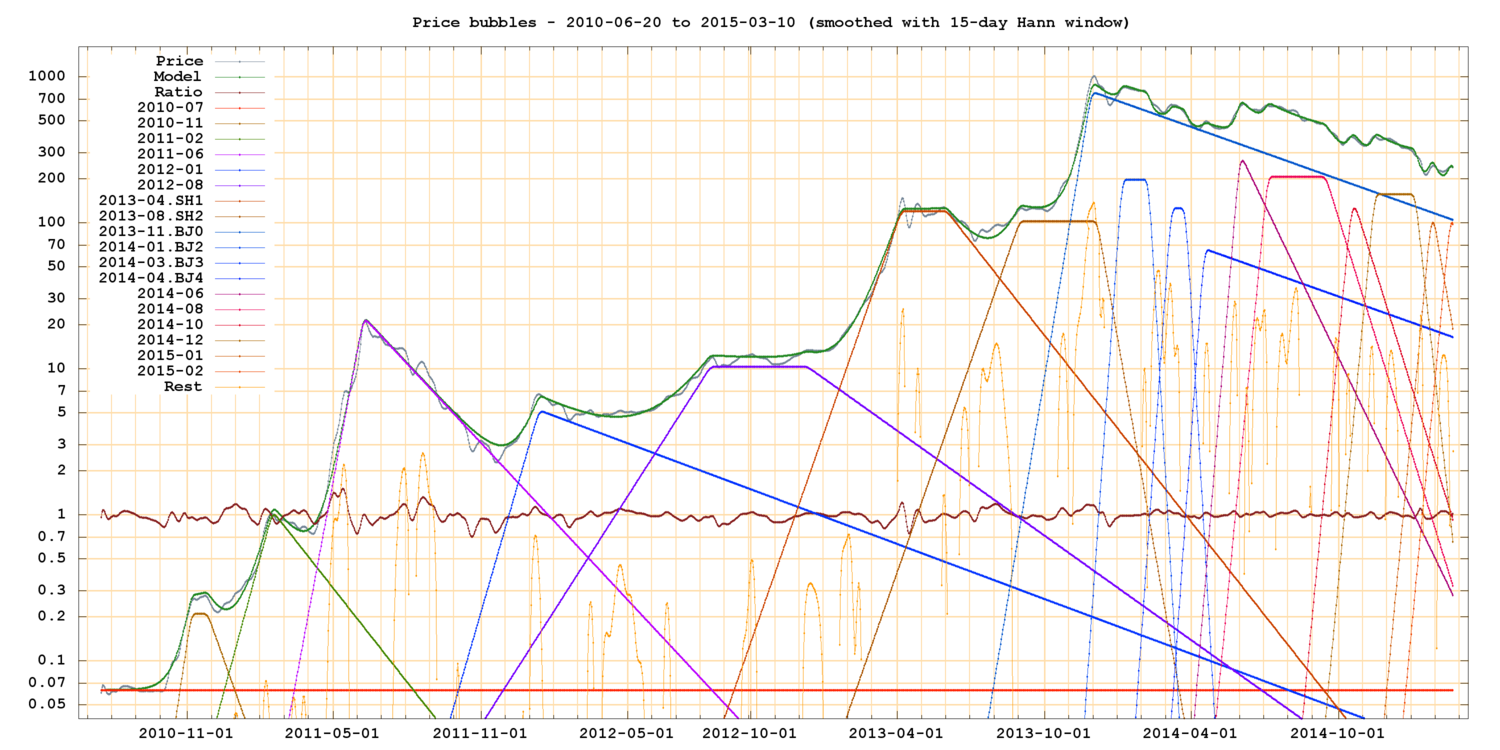

This plot show a model (green irregular line) for the historic series of daily BTC prices (gray irregular line) as the sum of "simple bubbles". The reddish-brown line at value about 1 is the ratio of the model and the actual price.

In each "simple bubble", the price grows exponentially with some rate r1 until a maximum value P at some date d1, then stays constant until some date d2, then decays with some rate r2. In most bubbles the dates d1 and d2 are equal, so there is no flat part between the exponential rise and the exponential decay.

The model is the sum of several of those "simple bubbles", each with its own parameters r1,d1,P,d2,r2. They are the triangular or trapezoidal lines in the plot.

Although each "simple bubble" mathematically extends infinitely in the past and in the future, it is relevant only for some limited interval of dates that includes d1 and d2. Outside that interval, it is too small compared to the sum of the other bubbles, and it could even be assumed to be zero, without a perceptible change in the model.

I believe that each "simple bubble" in this model, or set of consecutive bubbles, corresponds to the opening of some market, distinguished by geography, national borders, application, community, etc. For example, the two "simple bubbles" labeled "SH1" and "SH2" are probably due to surges of demand in China created by BTC-China in Shanghai. The four "simple bubbles" labeled "BJ0" to "BJ4" are almost certainly due to the adoption of bitcoin by the amateur commodity speculators in Mainland China, especially via OKCoin and Huobi in Beijing. Bubble "BJ0" models the basic demand of that market, while bubbles "BJ2" to "BJ4" model the extra demand that was turned on and off by the PBoC rumors and anti-rumors in early 2014.

The "simple bubble" model does not try to reproduce the oscillations of the price that occur at the end of a sharp rise.

The parameter P of each bubble represents its contribution to the price between d1 and d2. It is not proportional to the demand of BTC by the corresponding market, because the effect on price of a given demand depends on the amount of BTC available for trading, and that amount must have been decreasing as the price increased.

In the log plot, the exponential rise and fall of each bubble, plotted by itself, are straight diagonal lines; the rates r1 and r2 define their slopes. When the bubbles are added together, however, the rise and fall get distorted, and appear curved in the plot.

The raw prices (gray line) are the weighted mean prices in each UTC day. These raw prices and the simple bubbles were smoothed with a 15-day Hann window.